Many internal controls are still executed manually, even though the underlying business processes are already digital.remQ helps organizations transform manual checks into automated monitoring, structured alerts, audit trails, and continuous control assurance.

Internal Controls are essential for reliable financial reporting, compliance, fraud prevention, and strong governance. But in many organizations, the way controls are executed has not kept pace with the speed and complexity of modern business operations.

Business processes are increasingly digital, fast-moving, and data-driven. Yet many controls are still performed manually. Control owners download reports, review spreadsheets, check samples, collect approvals by e-mail, and upload evidence into separate repositories.

This creates a growing gap between control effort and control confidence.

Internal controls automation helps organizations close that gap. Instead of relying solely on periodic manual reviews, companies can continuously monitor transactions and master data, detect exceptions automatically, and document control execution in a structured, audit-ready way.

remQ is designed for organizations running SAP. It automates controls over business transactions, master data, and compliance-relevant activities directly inside the SAP environment, helping teams reduce manual effort, improve transparency, and strengthen audit readiness.

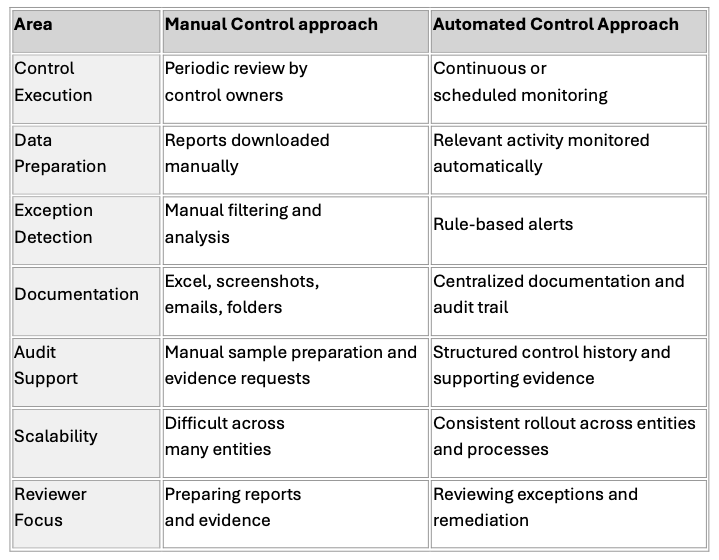

Manual controls are still common because they are familiar. They are often built around existing reports, spreadsheets, e-mail approvals, and document repositories.

A typical manual control process may look like this:

This approach can work for a limited number of controls, entities, and reviewers. But it becomes difficult to manage when the same controls must be executed across multiple company codes, countries, shared service centers, and/or business units.

The issue is not the control objective itself. Most control objectives are valid and important. The real problem is the manual operating model behind them.

Evidence is stored in different locations. Documentation quality varies between teams. Review steps depend heavily on individual control owners. Audit requests create additional workload. Exceptions are often identified after the fact. Management has limited visibility into whether controls are operating effectively.

For Internal Controls, ICS, SOX, Compliance, Finance, and GRC teams, this creates an uncomfortable situation: more time is spent performing and documenting controls, but assurance does not always improve at the same pace.

Internal controls automation means using system-based rules, monitoring logic, alerts, workflows, and evidence capture to identify risks, exceptions, or policy deviations with less manual effort.

It can support controls such as:

The goal is not to remove business judgment.The goal is to remove repetitive manual work and give control owners betterinformation, faster.

A manual control often asks:

“Did someone review the report?”

An automated control asks:

“Are defined risk conditions monitored continuously, and are exceptions detected, documented, and followed up?”

That is the real shift.

Internal Controls Automation helps organizations move from manual documentation toward digital internal controls, continuous control monitoring, and more structured assurance.

Traditional controls are often performed after the fact. A monthly report is downloaded, reviewed, documented, and stored. If an issue occurred at the beginning of the month, it may only be identified weeks later.

Continuous control monitoring changes this logic.

Instead of waiting for a periodic review, defined risk conditions can be monitored automatically. When an exception occurs, an alert is generated. The reviewer receives the relevant business context, investigates the case, documents the decision, and retains the evidence in one place.

This turns the control process from are curring administrative task into an ongoing assurance mechanism.

For control teams, this creates three important advantages.

First, exceptions can be identified earlier. Second, control execution becomes more consistent. Third, audit evidence is captured as part of the process instead of being reconstructed later.

This is where internal controls automation creates practical value: not by adding another layer of documentation, but by making the control itself more efficient, transparent, and scalable.

A bank master data change control is a strong example of what automation means in practice. In a traditional manual process, control owners in each entity download banking master data change reports on a monthly basis. They review each change, validate whether it was appropriate, obtain confirmation where needed, document their work, and provide evidence to Internal Audit or External Audit.

This process is time-consuming. It is also difficult to standardize across entities. One team may document the review in Excel. Another may store screenshots. A third may rely on email confirmations. When auditors request evidence, the control owner has to gather and explain the documentation again. With remQ, this type of control can be transformed into automated monitoring.

Relevant bank master data changes are monitored directly in the system. Alerts can show who changed what, when the change happened, and which values existed before and after the change. Reviewers can drill down into the relevant details, document their assessment, add comments or supporting evidence, and retain the full audit trail centrally. The control no longer depends on every entity manually preparing the same report. Instead, the relevant business activity is monitored automatically, and the reviewer focuses on exceptions and decisions. That is the essence of internal controls automation: turning manual checks into structured, continuous monitoring.

Internal Controls Automation is most valuable when controls are recurring, data-driven, and linked to financial, operational, or compliance-relevant risks.

Typical use cases include business process controls, IT application controls, and ITGC-related monitoring activities.

Procure-to-pay processes often involve risks related to incorrect invoices, incomplete approvals, payment term deviations, sensitive master data changes, or payments outside defined thresholds.

Examples of controls that can be automated include:

Automation helps control owners move away from recurring manual report reviews and focus on relevant exceptions.

In the Order-to-Cash process, automated monitoring can improve transparency over receivables, credit-related changes, manual adjustments, and customer master data changes.

Examples include:

This allows Finance and Internal Controls teams to work more exception-based instead of manually reviewing large reports on a recurring basis.

In Record-to-Report and General Ledger processes, manual journal entries, sensitive accounts, late reversals, and unusual postings are common focus areas for internal controls and external audit.

Automated controls can include:

The value is that control owners spend less time preparing reports and more time reviewing meaningful exceptions.

Fixed asset and procurement scenarios are also strong candidates for automation, especially when purchase orders, asset master data, delivery dates, and postings need to be monitored together.

Examples include:

These controls help identify process deviations earlier and improve documentation for Finance, Controlling, and audit teams.

Many internal controls are embedded directly into business processes as IT Application Controls (ITAC) These may include automated checks, tolerance limits, mandatory fields, approval logic, or system-based validations.

By automating the monitoring of ITACs and tracking master data changes and exceptions, remQ enhances transparency and verifies that process-integrated controls are functioning correctly. This improves transparency over whether process-integrated controls are operating as intended.

In addition to business process controls, ITGC-related monitoring activities are also relevant, especially where they affect the reliability of key reports, data, or automated controls. Examples of how remQ supports these areas include:

The important distinction is that remQ is not only an IT controls tool. Its main focus is the automation and monitoring of internal controls over business transactions and master data, complemented by ITGC- and ITAC-related use cases where they are relevant for the control environment.

The key point is not that automation removes people from the control process. It removes repetitive manual tasks so that people can focus on higher-value review activities.

remQ is an internal controls automation, compliance, and monitoring solution for organizations running SAP. It is embedded in the SAP environment and supports control execution, documentation and monitoring.

Rather than acting only as a control repository, remQ helps automate the actual monitoring and execution of controls over business transactions, master data, and compliance-relevant activities.

Not every control needs to run in real time. Some controls are better designed as scheduled checks, for example weekly, monthly, or quarterly.

remQ supports both real-time and scheduled monitoring. This allows organizations to design controls based on risk, business criticality, and review capacity.

A high-risk master data change may require immediate alerting. A recurring completeness or reasonableness check may be better suited to a scheduled control run. The important point is that the control frequency can be aligned with the business risk instead of being limited by manual review cycles.

Organizations rarely start internal controls automation from the same point. Some want to automate existing manual controls quickly. Others already have a mature control framework and need company-specific logic for local requirements, SOX-relevant processes, regulatory expectations, or internal policies.

remQ supports these different starting points through a modular control automation platform.

Organizations can select and activate exactly what they need from a library of more than 120 best-practice controls. This allows teams to tailor the automation to their specific risk profile and scope, covering key areas such as Procure-to-Pay, Order-to-Cash, Record-to-Report, General Ledger, Fixed Assets, HR, ITGCs, and compliance monitoring. By choosing from these pre-configured templates, Internal Controls, Compliance, and Finance teams can move faster and avoid the need to design every control from scratch, while ensuring the solution remains focused and manageable.

At the same time, remQ is not limited to predefined control content. With its configurable no-code rule engine, organizations can adapt controls to company-specific thresholds, approval limits, risk indicators, process variants, and local requirements. They can also create new controls for unique risks, regulatory needs, or custom business logic.

This creates three practical usage models:

All approaches operate on a unified SAP-native platform. This allows control logic, alerts, responsibilities, documentation, dashboards, and audit trails to be managed consistently. For Internal Controls and Compliance teams, remQ becomes a scalable platform that supports both standardization and flexibility.

Control automation only creates value if the results are understandable and actionable. Whenever a control identifies a transaction or data change that matches a predefined rule or exception, an "alert" is generated. This alert acts as a targeted notification, signaling that a specific case requires review.

To ensure efficient processing, remQ alerts include full business context such as Transaction Details: Company code, document number, vendor, and amounts.

This level of detail helps reviewers understand the exception quickly and decide whether follow-up action is required. Furthermore, control results are visualized in dashboards and KPI summaries, giving Internal Controls, Compliance, Finance, and GRC teams transparency over control performance, open alerts, recurring exceptions, and remediation status.

To close the loop, responsibilities are assigned to designated users or roles. This ensures clear ownership for the review, documentation, and follow-up of every generated alert.

The business case for internal controls automation is strongest where controls are recurring, manual effort is high, and exceptions have financial or compliance relevance.

Control owners spend less time downloading reports, preparing spreadsheets, saving screenshots, and collecting evidence.

This allows them to focus on reviewing exceptions, understanding root causes, and improving the underlying process.

The same rule logic can be applied across entities and processes. This reduces variation in how controls are performed and documented.

For global organizations, this consistency is especially important. A control should not depend on local spreadsheet formats or individual documentation habits.

When evidence is captured as part of the control process, audit preparation becomes less reactive. Audit teams can work with structured control histories instead of chasing individual files and explanations.

This can reduce the time spent on sample preparation, evidence collection, and repeated clarification requests.

Continuous control monitoring helps identify risk events closer to the time they occur. This supports faster investigation and remediation.

Instead of finding an issue weeks after a manual review, teams can act earlier and reduce the potential impact.

Controls such as duplicate invoice detection, payment terms validation, and master data monitoring can help identify preventable losses and process weaknesses.

The value is not only in detecting individual exceptions. Over time, recurring patterns can help management understand where process improvements are needed.

Automated controls give Internal Controls, Compliance, Finance, and GRC teams better transparency over what is happening in critical business processes.

This helps internal control systems become more than a compliance requirement. They become a practical steering mechanism for better governance and operational resilience.

Organizations do not need to automate the entire control framework at once. A focused starting point is usually more effective.

1. Identify controls with high manual effort

Look for controls that require recurring report downloads, spreadsheet analysis, manual documentation, and repeated audit support.

These controls often offer the fastest efficiency gains because the manual workload is visible and recurring.

2. Prioritize controls with clear business risk

Good candidates are controls linked to financial leakage, fraud risk, compliance exposure, recurring findings, or high audit effort.

Examples include vendor bank data changes, duplicate invoices, payment terms deviations, journal entry reviews, and sensitive master data changes.

3. Choose controls with clear logic

Automation works best when the control logic can be clearly defined. Examples include specific fields, thresholds, document types, company codes, date deviations, duplicate criteria, or change events.

If the logic is too vague, the automation may create too many alerts or require too much manual interpretation.

4. Define ownership and review workflow

Automation should not only generate alerts. It should also define who reviews them, what evidence is required, how decisions are documented, and how remediation is tracked.

Clear accountability is essential. Without it, automated alerts can become another unmanaged worklist.

5. Scale gradually

Start with a few high-value controls, prove the benefit, and then expand to additional processes, entities, and risk areas.

Good starting points often include bank master data changes, duplicate invoice detection, journal entry monitoring, and high-risk master data changes.

Automation can create significant value, but only if the control design is clear.

Automating the old manual process without redesigning it

A poor manual control does not become a good control simply because it is automated. The risk, objective, logic, and evidence requirements should be reviewed first.

Creating too many alerts

If the control logic is too broad, reviewers may receive too many false positives. Automation should help teams focus, not overwhelm them.

Alert quality is critical. A smaller number of relevant alerts is usually more valuable than a large number of low-quality exceptions.

Treating automation as an IT-only project

Internal Controls, Compliance, Finance, business process owners, and IT should work together.

The business defines the control objective and risk logic. IT supports the technical implementation. Internal Audit can provide input on evidence expectations and auditability.

Ignoring audit evidence requirements

Automation should not only detect exceptions. It should also support documentation, review history, approval, and auditability.

If evidence requirements are not considered from the beginning, teams may still need manual workarounds later.

Internal controls automation helps organizations move from manual, periodic, and fragmented control execution to continuous monitoring and structured assurance.

The opportunity is clear: many business processes are already digital, but the controls around them are still manual. By automating control execution, monitoring, alerting, documentation, and audit trails, organizations can reduce manual effort, improve consistency, detect exceptions earlier, and strengthen audit readiness.

remQ helps organizations make this shift. It transforms manual controls into automated monitoring, supports control owners with structured alerts and audit trails, and enables Internal Controls, Compliance, Finance, Audit and GRC teams to work with greater transparency and efficiency.

For organizations that want to reduce control effort and increase control confidence, internal controls automation is a practical next step.

Internal controls automation means using system-based rules, monitoring logic, alerts, workflows, and audit trails to identify risks, exceptions, or policy deviations with less manual effort. It helps organizations move from manual report reviews to continuous control monitoring.

No. Automation does not replace control owners. It reduces repetitive manual work and helps control owners focus on exceptions, root causes, decisions, and remediation.

Good candidates include bank master data changes, duplicate invoice detection, payment terms validation, high-value payments, journal entry reviews, sensitive master data changes, fixed asset controls, and SoD-related activity monitoring.

No. remQ is not limited to IT controls. It supports automated controls over business transactions, master data, and compliance-relevant activities in organizations running SAP.

A practical starting point is to identify manual controls with high effort, clear business risk, and rule-based logic. Typical examples include bank master data changes, duplicate invoices, payment terms deviations, journal entry reviews, and sensitive master data changes.

Hast Du Fragen oder möchtest Du etwas hinzufügen? Hinterlasse uns bitte eine Nachricht! Deine Nachricht wird per E-Mail an uns übermittelt und nicht veröffentlicht.